Socially Responsible Investing with Wealthfront

Publication date: October 16, 2024. The information in this white paper is accurate as of this date. When we make material updates, we will also update the publication date.

Introduction

Wealthfront offers two types of fully managed, diversified, automated portfolios to clients: Classic portfolios and Socially Responsible portfolios. This white paper discusses the construction of Wealthfront’s Socially Responsible portfolios, which are designed to offer similar risk-adjusted returns as our Classic portfolios with a focus on socially responsible investing.

What is Socially Responsible Investing?

While socially responsible investing (SRI) doesn’t have a single agreed-upon definition, it’s generally seen as an investment strategy that evaluates companies based on their benefit and/or detriment to society, rather than profits or intrinsic value alone. This concept comes from an ethical framework called “social responsibility,” in which individuals and corporations have an obligation to cooperate with others to benefit greater society. Some investors may take up SRI strategies due to a long-term belief in its investment value, and others may decide to use this strategy purely due to ethics.

Since there’s no agreed-upon definition of SRI, investors evaluate which investments to include in an SRI strategy in a variety of ways. Some investors may take an exclusionary approach, avoiding stocks or bonds if the underlying company is involved in activities considered detrimental to society. For example, a fund manager building an SRI ETF (exchange-traded fund) might exclude stocks involved in fossil fuel extraction, firearms, or tobacco from their portfolio. At the other end of the spectrum, some investors may only invest in companies if their business activities agree with a particular set of values considered beneficial to society, an approach known as “impact investing.” Examples of impact investments include clean energy portfolios and a portfolio of companies committed to promoting diverse leadership. Investors may also combine elements of both strategies, excluding companies from certain industries and investing a relatively high fraction of the portfolio in companies whose businesses align with their values.

For Wealthfront’s Socially Responsible Investing portfolios, SRI means promoting social impact by selecting investments that increase exposure to companies receiving high scores on ESG factors.

What is ESG?

You may have heard the term “ESG” in relation to SRI. ESG stands for environmental, social, and governance — three pillars of corporate social responsibility. Each pillar contains specific factors on which companies can be measured.

Environmental factors take into account a company’s conservation efforts, scored on areas such as:

- Climate change

- Carbon emissions

- Air and water pollution

- Biodiversity

- Deforestation

- Energy efficiency

- Waste management

- Water usage intensity

Social factors take into account a company’s practices regarding people and relationships, such as its consideration of human rights, labor laws, and customer relationships. These measures are scored on areas such as:

- Diversity

- Human rights and labor standards

- Customer satisfaction

- Data privacy and protection

- Customer and employee relations

- Community relations

Governance factors take into account a company’s standards for management, scored on areas such as:

- Board composition

- Audit committee structure

- Executive compensation

- Lobbying and political contributions

- Whistleblower schemes, bribery and corruption

ESG Scoring

We use ESG-aware Blackrock funds as the primary funds in our Socially Responsible portfolios. These funds track socially responsible indices defined by MSCI, which also scores the underlying stocks or bonds on ESG factors.

Each company in the MSCI index is scored on a weighted collection of factors within the three ESG pillars, with criteria that vary by how important each factor is deemed to that company’s industry. For example, within the environmental pillar, companies in the soft drinks industry are scored on three factors — water stress, packaging material and waste, and carbon footprint, while companies within the healthcare services industry are scored only on carbon emissions.

Index Creation

With the ESG quality scores of the individual companies assigned, MSCI next determines the weight of each instrument in the relevant index. Companies in certain industries or that derive meaningful fractions of their revenue from activities deemed controversial by MSCI are excluded entirely. These industries include civilian firearms, controversial weapons, tobacco, thermal coal and oil sands, and the details can be found here. To determine the weights on the individual stocks or bonds, MSCI uses an optimization process designed to maximize the weighted-average ESG quality score of the portfolio, subject to constraints intended to keep the risk and return profile of the ESG index similar to that of a standard (non-ESG) index called the “parent index”, and to control trading from rapid weight changes. These constraints include:

- An upper bound on the expected tracking error between the ESG index and the parent.

- Maximum weights of individual companies relative to their weight in the parent.

- Maximum weights of sectors and countries relative to the parent.

- Upper bounds on total turnover. Turnover is defined as the sum of the magnitude of weight changes from the last definition to the current one.

Each fund in Blackrock’s suite of ESG-aware ETFs seeks to track the performance of a particular MSCI index. The overall ESG quality score of an ETF is simply the weighted average of the scores of its holdings on a range from 0 to 10, with 10 being the best. Note that while nearly all companies and funds are assigned scores by MSCI, there are certain companies and instruments that haven’t been scored. For example, municipal bond ETFs do not receive ESG ratings.

Choosing Asset Classes and Instruments

To help balance potential returns and impact, we generally choose ETFs that track indices favoring companies with higher overall ESG quality scores while maintaining low tracking error to the “standard” indices.

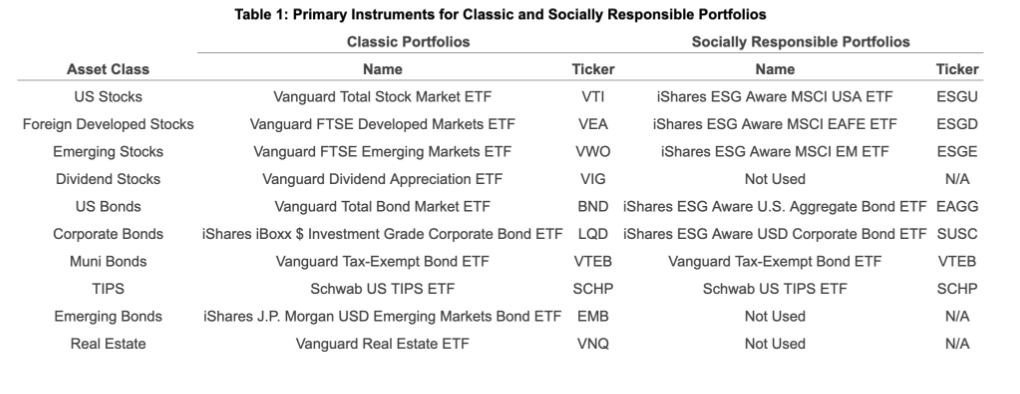

Each of the ETFs in our Socially Responsible portfolios represents a specific asset class, in line with our implementation of Modern Portfolio Theory (which is described at length in our Classic Portfolio Investment Methodology white paper). Table 1 shows the asset classes represented in each set of portfolios, as well as the ETFs selected to represent each asset class.

While we do our best to find socially responsible ETFs for every part of your portfolio, not all asset classes have adequate socially responsible ETFs that can be used to represent them. In some cases, we choose to remove the unrepresented asset class entirely, such as with Dividend Stocks, Emerging Bonds, and Real Estate. In other cases, like with Municipal Bonds and Treasury Inflation-Protected Securities (TIPS), we use the same ETF employed by our Classic portfolios. Although these ETFs are not explicitly designed to adhere to SRI principals, bonds issued by the US government and municipalities fund beneficial spending such as infrastructure, schools, and social programs. Moreover, TIPS and municipal bonds aid in diversification and tax-efficiency.

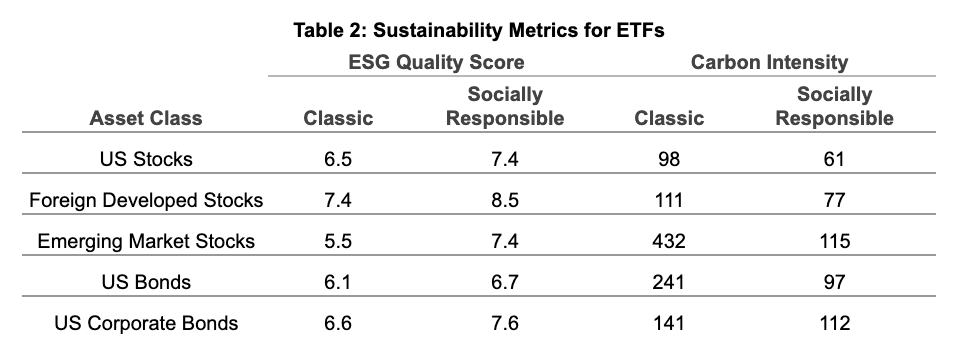

In addition to the overall ESG quality score, we highlight a second sustainability metric, which scores companies based on their carbon emissions. This metric, called carbon intensity, is calculated by MSCI and captures the tons of carbon dioxide emitted by each company, per million dollars in sales. We don’t use this metric when selecting ETFs or in portfolio construction, but we find that it is an informative and tangible measure that the Socially Responsible portfolios tend to improve upon. As with the ESG quality score, the carbon intensity score for an ETF is the weighted-average score of its holdings. Table 2 compares the ESG quality scores and carbon intensity scores between ETFs used in our Classic portfolios and Socially Responsible portfolios for the asset classes with socially responsible variants. Note that a more socially responsible fund will have a higher ESG quality score and a lower carbon intensity score. The ETFs used in our Socially Responsible portfolios score significantly better than those used in our Classic portfolios on both ESG quality and carbon intensity.

Constructing Portfolios

Expected Returns and Covariance Matrix

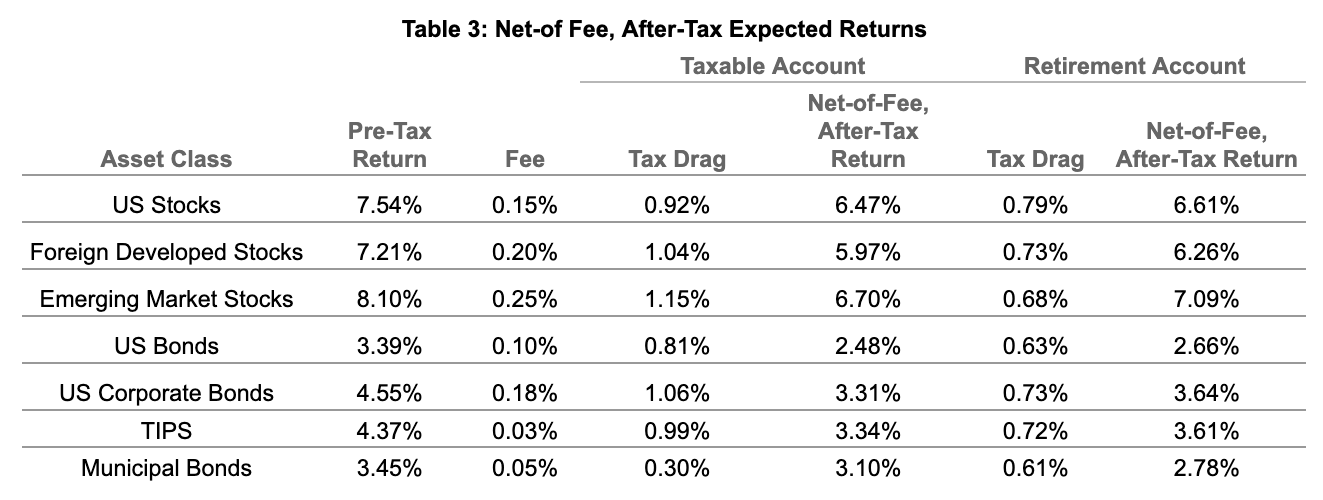

Once we have decided on the asset classes and instruments to employ in the Socially Responsible portfolio, we choose weights for each instrument in the overarching portfolio. To do this, we use the same process described in our Classic portfolio investment methodology white paper: We first estimate each asset class’s pre-tax pre-fee expected returns and the variance-covariance matrix across asset classes. Next, we estimate how much of the pre-tax expected return is likely to be lost to taxes (i.e. tax drag) on an annualized basis. We then subtract the tax drag and the ETF’s expense ratio from the pre-tax pre-fee expected return to arrive at net-of-fee, after-tax expected return for each asset class. Finally, we use after-tax expected returns and the covariance matrix as inputs to the mean-variance optimization process designed to provide a collection of portfolios that seek to generate the maximum after-tax expected return at each level of targeted risk.

To estimate tax drag, we estimate:

- For each asset class, the fraction of the expected return that could be distributed each year, either in the form of income (dividends, interest) or capital gains. Given the low index turnover and the tax efficient nature of ETFs, we assume capital gain distributions are zero, which is consistent with historical data. The fraction of income distributed is estimated based on historical dividend yields.

- For each asset class, the fraction of dividend distributions that will be treated as qualified, and thus may be subject to taxation at the lower long-term capital gains rates instead of income rates. This is estimated based on historical data.

- For each account type (taxable or retirement), the projected time until liquidation (10 years for taxable and 30 years for retirement accounts), which is necessary to amortize the taxes due at liquidation (capital gains in taxable accounts, and ordinary income in traditional retirement accounts) over the life of the investment.

We simulate the pre-tax returns of each asset class, apply the relevant tax rules within the two account types, and then compute the net-of-fee, after-tax return. This methodology allows us to assess the combined impact of taxes on the intermediate distributions, as well as the liquidation of the account. The difference between the annualized pre-tax and after-tax returns captures the tax drag.

Table 3 shows the pre-tax expected return, tax drag i.e. the amount of return lost to taxes annually, and net-of-fee, after-tax expected returns for each asset class. For illustrative purposes, we assume a combined ordinary income tax rate of 28% (24% federal + 4% state), applicable to Wealthfront’s median client weighted by assets. We further assume the household is subject to a 15% federal long-term capital gains rate and a 24% federal short-term capital gains rate. (Note that for our Socially Responsible portfolios, we optimize our tax assumptions based on information such as your tax filing status, annual household income, and state of residence. We explain this in more detail in the Personalization with Tax Rates section below.) Thus, for each year, tax paid is the amount of non-qualified dividends and interest multiplied by the ordinary income rate of 28%, plus the amount of qualified dividend multiplied by the long-term capital gain rate of 19% (15% federal + 4% state). For the final year of your investment horizon when we assume you liquidate your investments, you would also pay 19% on your capital gains for taxable accounts and 28% for income from retirement accounts. The final tax drag number looks at the total amount of tax paid over the full investment horizon and arrives at an annualized amount to be deducted from your annual expected return.

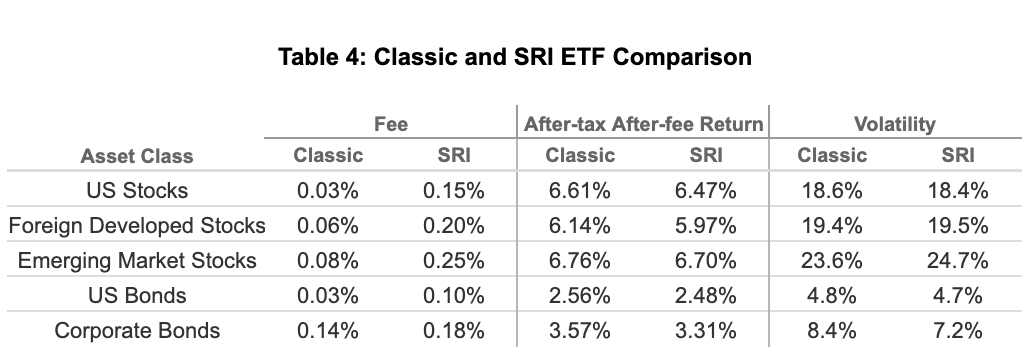

Table 4 compares the fees, expected returns, and volatilities of the ETFs used in Classic portfolios with those used in the Socially Responsible portfolios. We use the same tax rate assumptions we used for taxable portfolios in Table 3 for this example. We can see that socially responsible ETFs generally have slightly lower after-tax, after-fee return, primarily due to the higher fees the socially responsible ETFs typically charge. For corporate bonds, the socially responsible ETF generally has a slightly shorter duration (a measure of sensitivity to interest rates), which can result in lower volatility and lower expected return. The ETF used to represent emerging markets stocks in the Socially Responsible portfolios has a higher volatility due to having slightly different country exposures compared to the fund used in the Classic portfolios. Overall, the ETFs chosen for Classic and Socially Responsible portfolios aim to have similar risk and expected return characteristics.

Personalization with Tax Rates

For taxable accounts, Wealthfront optimizes our asset allocation recommendation based on your federal and state tax rates, in an effort to maximize your portfolio’s after-tax expected return while maintaining an appropriate level of risk.

The optimization considers differences in tax implications for different asset classes. Interest from municipal bonds is typically exempt from federal tax. It is also often exempt from state tax if the municipal bonds are issued by your state of residence. Interest from Treasury bonds, including TIPS, is typically exempt from state tax. All else being equal, bonds with more tax exemptions tend to have lower pre-tax returns, and are therefore more appealing to investors with higher marginal tax rates. We also consider tax rate differences for gains from different sources in our after-tax expected return calculation, which informs the objective of our mean-variance optimization: Income such as dividends and interest, as well as short-term capital gains, are taxed at ordinary income rates, whereas “qualified” dividends and long-term capital gains are taxed at the lower long-term capital gain rates.

For most states, we use a “national” municipal bond ETF holding bonds from states across the country. For states with high tax rates, we will consider state-specific municipal bond ETFs if they meet our liquidity and cost criteria and may offer the potential to improve after-tax, after-fee expected returns. Currently, California is the only state which meets these criteria. We’ll discuss our approach to creating California-specific allocations in the next section.

There are seven federal marginal income tax brackets, ranging from 10% to 37%. State income tax can vary widely across states. Several states such as Florida, Washington, and Texas do not have a state income tax at all. Other states have maximum rates of 8% or higher, with California topping the list with rates up to 13.3%. As our portfolio optimization’s objective is to maximize after-tax expected return of the portfolio, different tax rates will impact the after-tax expected returns used in the objective, and potentially result in different allocations. However, we find that the optimal portfolio allocations are insensitive to the exact choices of tax rates. In fact, our research demonstrates that three representative portfolios—each optimized for a specific combination of state and federal taxes—are generally sufficient to deliver an expected after-tax return within 0.02% of the optimal return for any combination of tax rates.

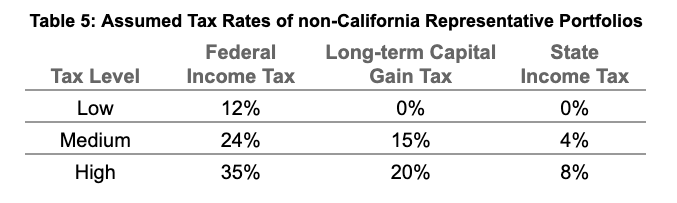

Table 5 shows the assumed state and federal tax rates used in each of the three representative portfolios for non-California residents. For the high tax level portfolio, we chose 35%, the median of the three highest federal tax rates of 32%, 35% and 37%. For long-term capital gain tax rates, there are a total of three rates: 0%, 15%, and 20%. We picked 20% for high tax level portfolios. For state tax, the number varies across states, with California’s 13.3% as the maximum. We chose 8%, which is slightly lower than the midpoint between 4% and 13.3%, as only two states, New York and California, have state tax rates above 10%. In the next section, we will recommend a specific allocation for California residents, which leaves New York as the only state with rates above 10% for the non-California allocations. For the low tax level portfolio, we chose 12%, the median of the three lowest federal income tax rates of 0%, 12%, and 22%. For the long-term capital gains tax rate, we chose the only option below 15%, which is 0%. For state tax, we also chose 0% to be sufficiently different from 4% and to better represent states where there is no state income tax.

As of November 2024

In order to find the most tax-efficient portfolio for you, we first infer your marginal federal and state income and long-term capital gain tax rates based on your responses to the following three questions: your tax filing status, annual household income, and state of residence. We use marginal tax brackets because any realized earnings from the Automated Investing Account will be in addition to the annual income you already earn. We also assume a standard deduction from annual income when inferring the tax brackets. We then calculate your after-tax expected return for each of the three representative portfolios, and assign you to the portfolio that aims to deliver the best expected return. Table 6 shows the assigned portfolio for every possible combination of state (rounded to the nearest percent) and federal income tax rates based on this methodology. Long-term capital gains tax is not included in the mapping because in most cases the income range for a specific federal income rate maps uniquely to one long-term capital gain tax rate. In the few cases where there are two possible long-term capital gain tax rates, their optimal portfolio choices are the same.

Allocations for California residents

We offer special allocations for residents of California. California is unique among states because:

- It has very high tax rates—its top marginal rate of 13.3% is the highest in the country.

- There is a liquid and low-cost ETF (for example, we use the iShares California Muni Bond ETF, with an expense ratio of 0.08%) dedicated to municipal bonds issued in California.

Remember that interest from municipal bonds issued in your state of residence is exempt from state taxes as well as federal taxes. This exemption, along with the availability of the California-specific municipal bond ETF, allows us to create portfolios that strive for higher after-tax, after-fee expected returns for California residents—especially those in the highest tax brackets.

We take a holistic approach to our California customization. Instead of simply replacing the broad US municipal bond weight in the non-California allocations, we use the same mean-variance optimization approach in an attempt to arrive at the optimal portfolios. This way, we are able to take into account California municipal bonds’ specific after-tax, after-fee expected return, as well as their volatility and correlations with other asset classes.

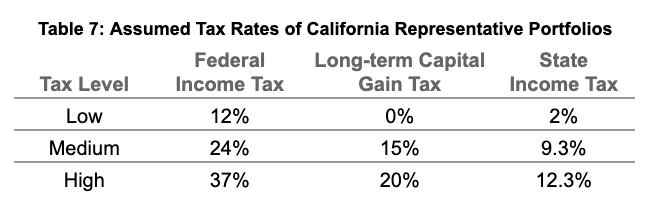

For California residents, our research demonstrates that three representative portfolios may be sufficient to deliver an expected after-tax return within 0.03% of the optimal return for any combination of tax rates. In Table 7, we show the assumed tax rates for these representative portfolios, which reflect California state tax rates. The tax rates are higher than non-California ones due to California’s higher state tax rates.

Rebalancing and Ongoing Management

Our SRI portfolios are managed using the same process as our Classic portfolios, including tax-loss harvesting, dividend reinvestment, and tax-efficient rebalancing and withdrawals.

Every ETF used in our SRI portfolios is eligible for tax-loss harvesting, meaning that Wealthfront clients choosing our SRI option in a taxable account still get the full benefit of our tax-loss harvesting service. Table 6 shows the primary and secondary ETFs used for each of the five asset classes where socially responsible funds are available. Each alternate ETF is highly correlated with the primary ETF used to represent the asset class.

As of November 2024

We use the methodology described previously in an effort to find the optimal portfolio for each possible state and federal tax rate combination. Long-term capital gains rates are also not included here because they do not impact the portfolio choices.

Taxable and Retirement Allocations

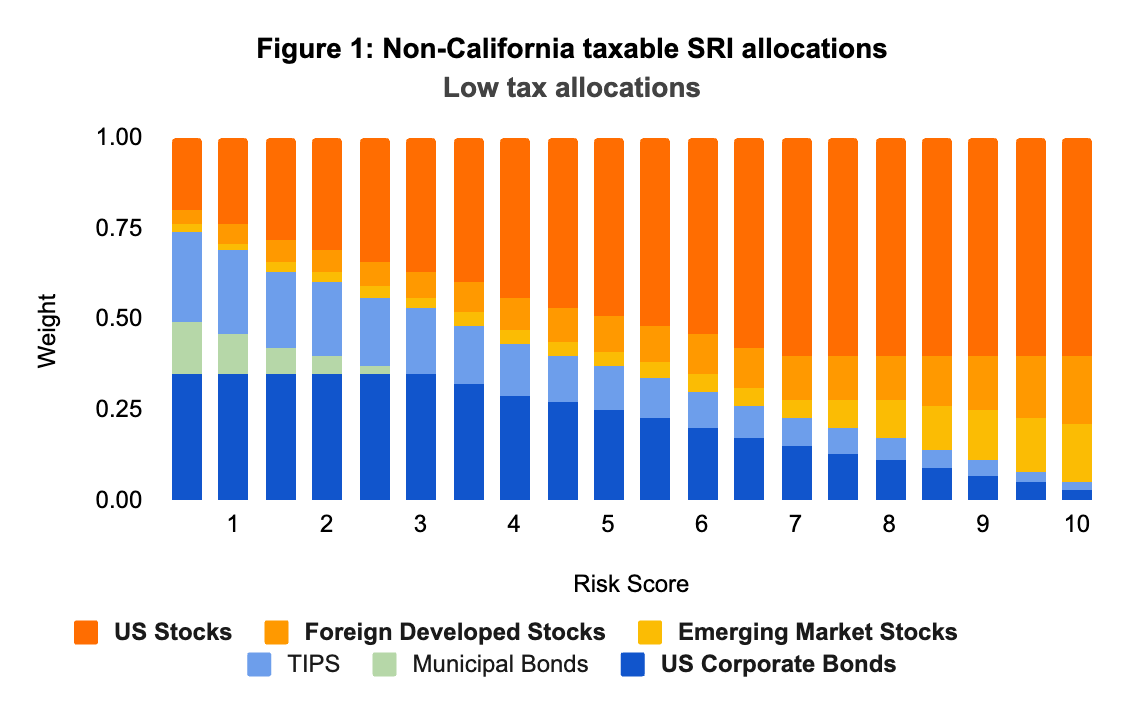

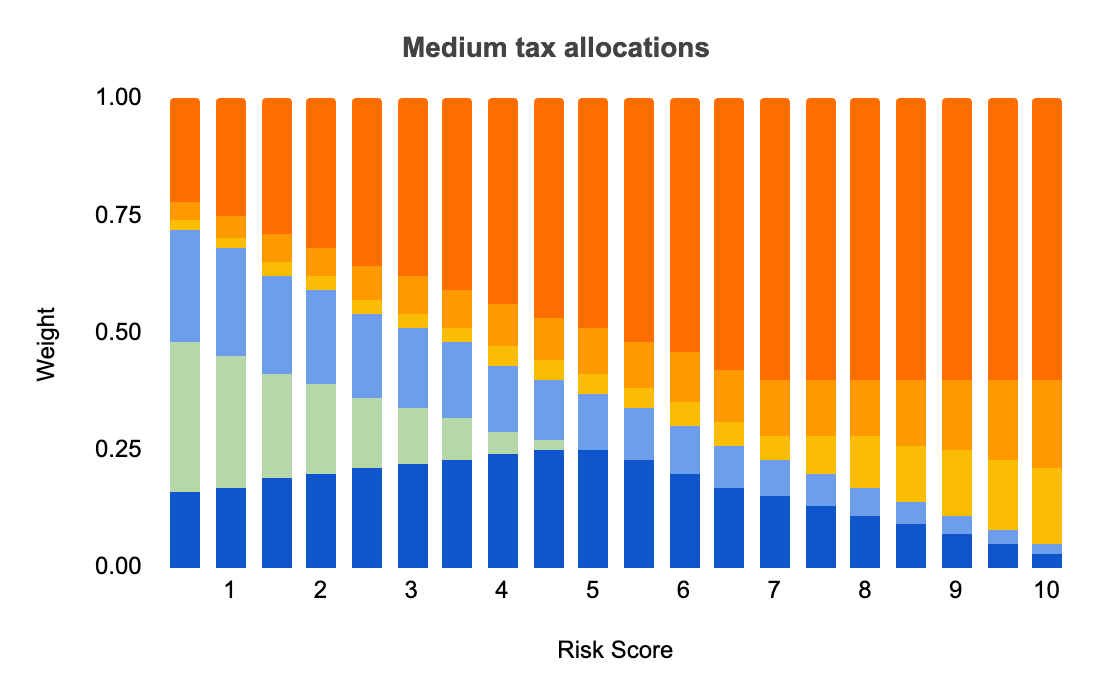

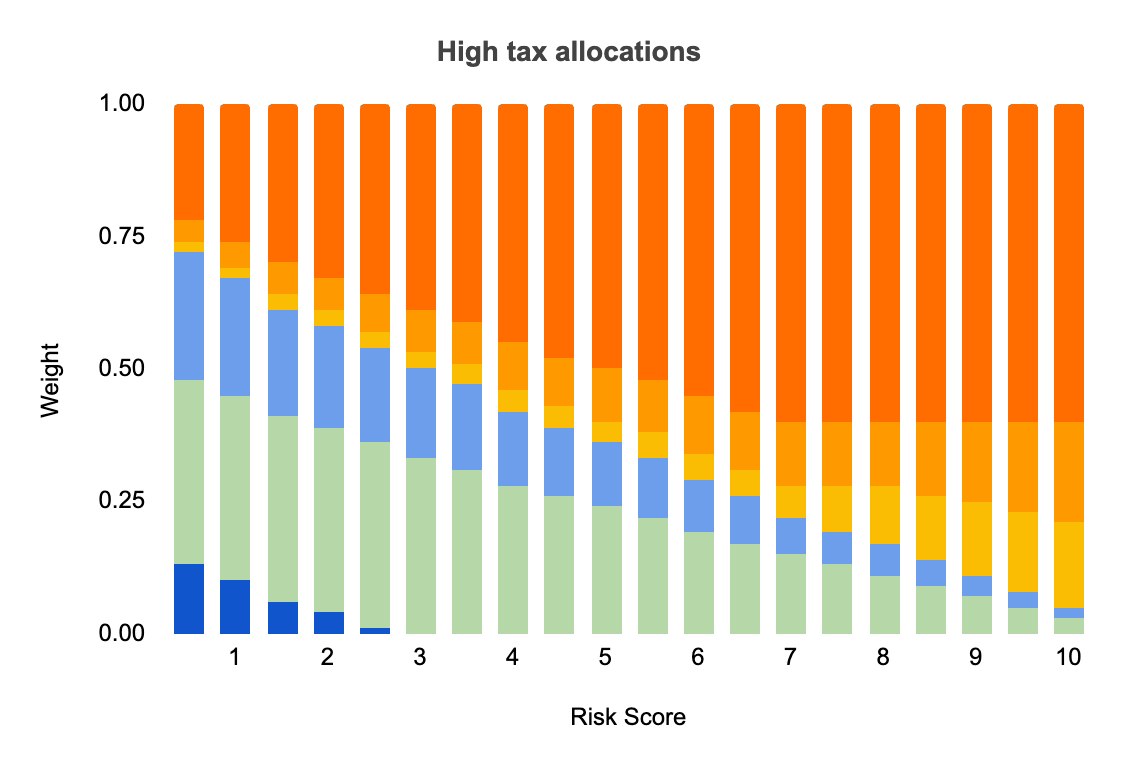

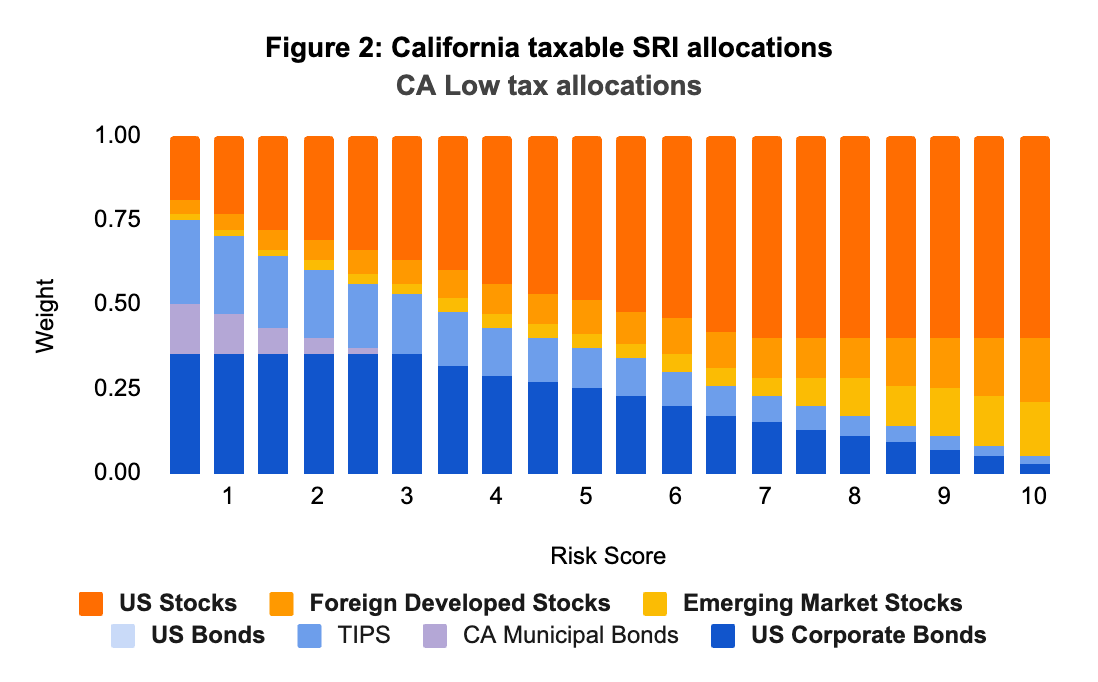

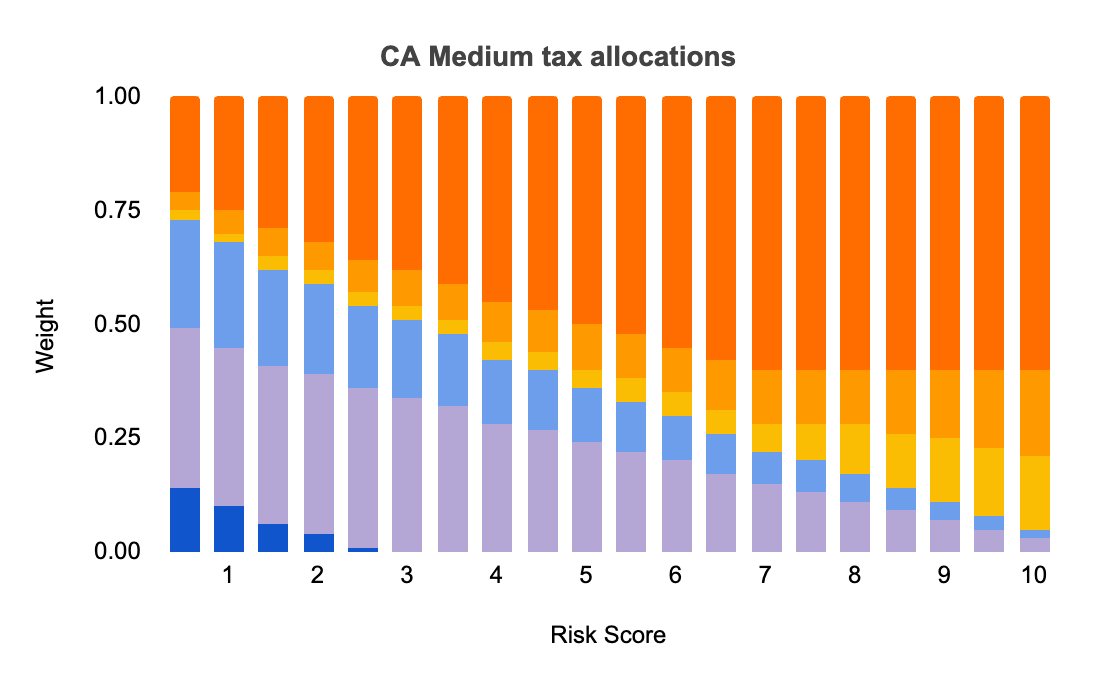

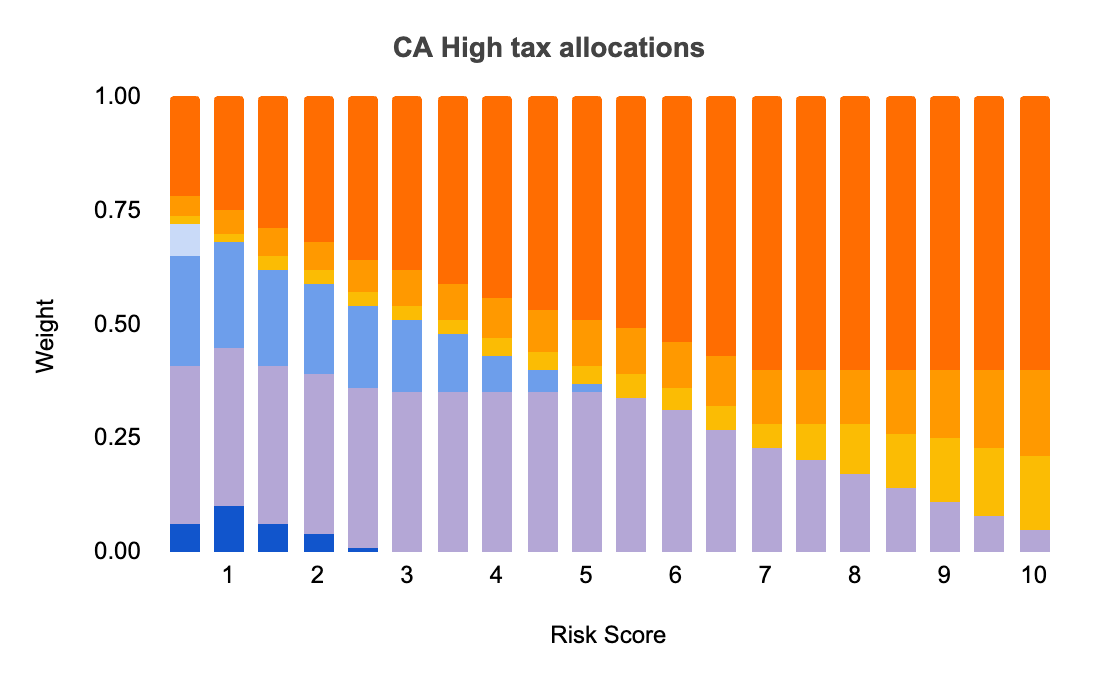

The final weights of each Socially Responsible portfolio are shown in Figures 1, 2 and 3, for non-California taxable, California taxable, and IRA accounts, respectively. The two taxable types also show low, medium, and high tax level allocations. Asset classes represented by socially responsible ETFs are shown in bold type.

Figure 1 presents the optimal allocations for non-California socially responsible taxable accounts. Depending on the targeted risk level and assumed tax rates, the portfolios contain either five or six asset classes. As assumed tax rates increase, the allocations include more municipal bonds as their federal tax exemption becomes more valuable. As risk level increases, the weights of lower risk and lower return fixed income asset classes such as municipal bonds and TIPs decrease, whereas higher risk and higher return equity asset classes weights increase.

Figure 2 presents the allocations for taxable accounts held by California residents. The patterns here are largely similar to what we saw with the non-California portfolios: As tax rates increase, the portfolios include more California municipal bonds to take advantage of the federal and state tax exemptions, and as risk scores increase, the portfolios hold more equities and fewer bonds.

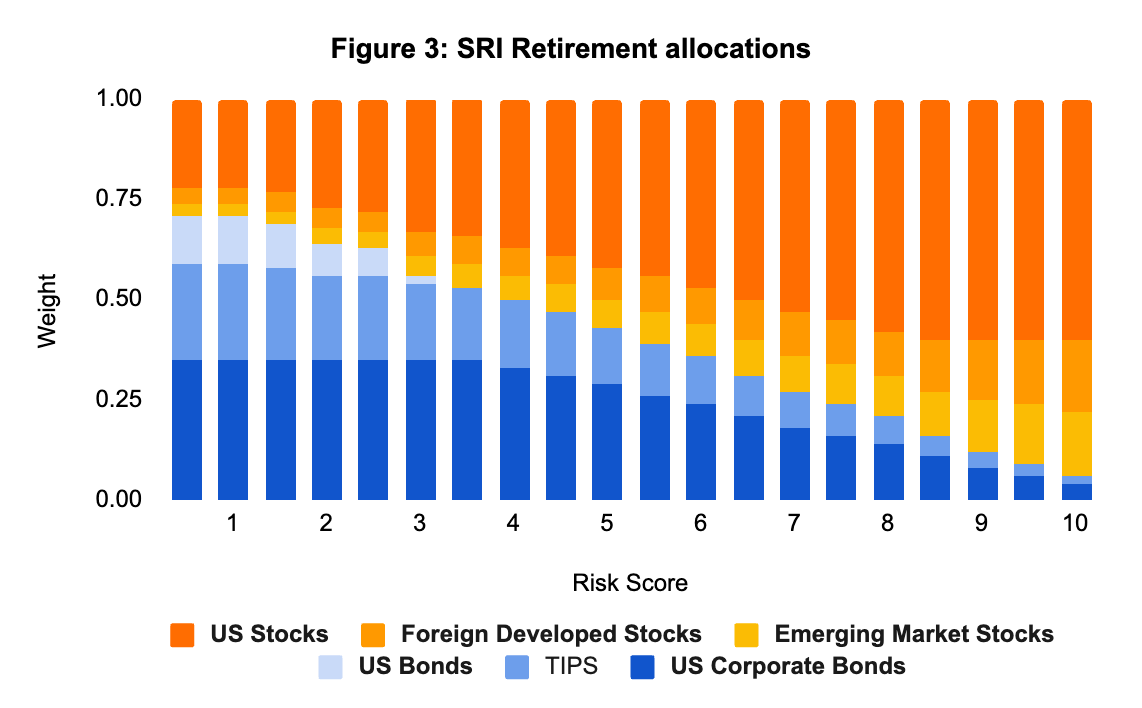

Figure 3 represents the optimal asset allocations for socially responsible retirement accounts. Because retirement accounts, like a traditional IRA, are tax-deferred, tax rate optimization does not offer meaningful benefits to these accounts, so we offer only one set of allocations by varying target risk levels. Similar to the taxable allocations, the portfolios include more equities and fewer bonds as the targeted risk level increases. Municipal bonds are not included in retirement allocations, as their tax exemptions do not have meaningful benefits in these accounts.

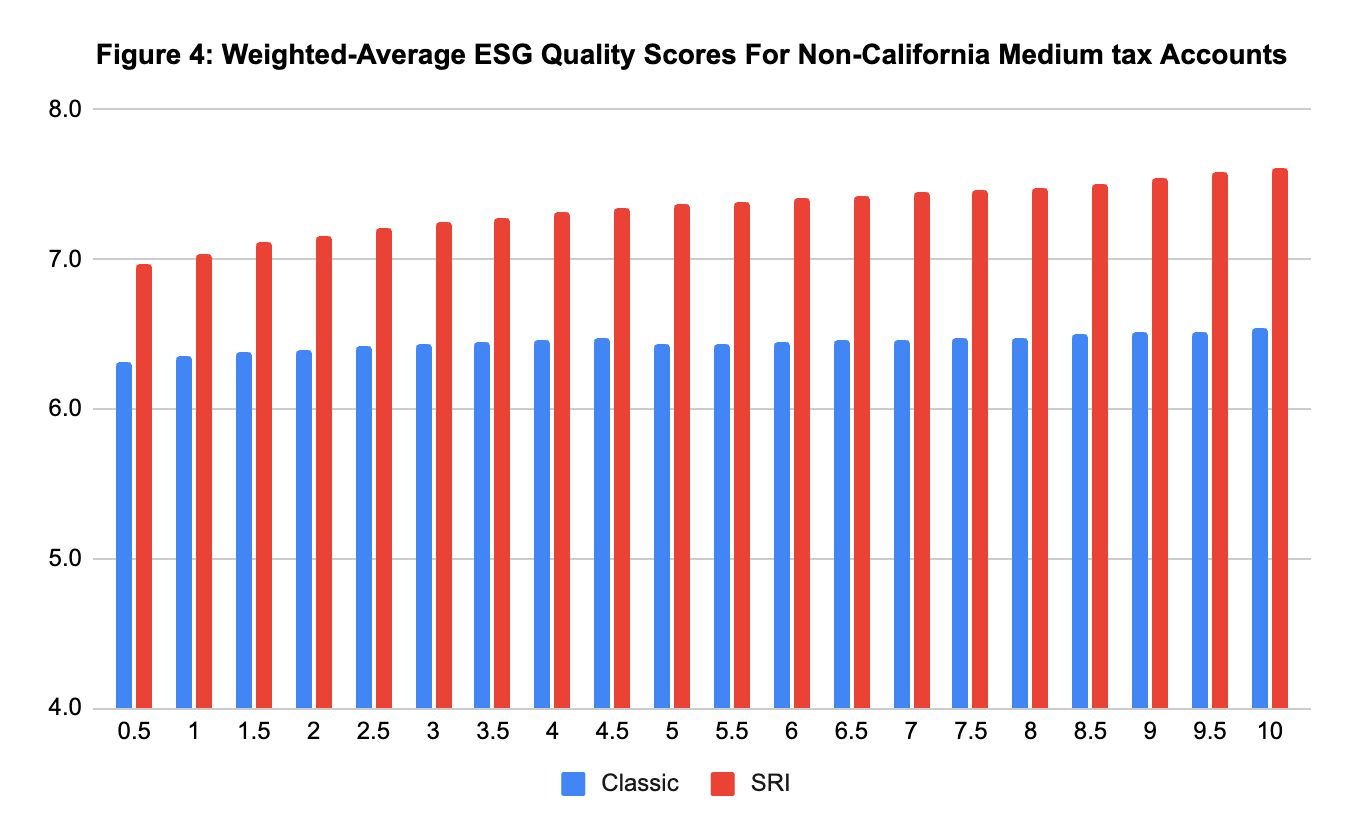

The substitution of socially responsible ETFs into these portfolios improves their sustainability characteristics substantially. To get a portfolio-level score for the ESG quality and carbon intensity metrics mentioned previously, we take a weighted average, excluding municipal bonds (municipal bond ETFs do not receive ESG scores). Figure 4 shows the ESG score comparison between Classic and Socially Responsible portfolios for non-California medium tax level accounts. Across risk scores, Socially Responsible portfolios have consistently higher ESG scores.

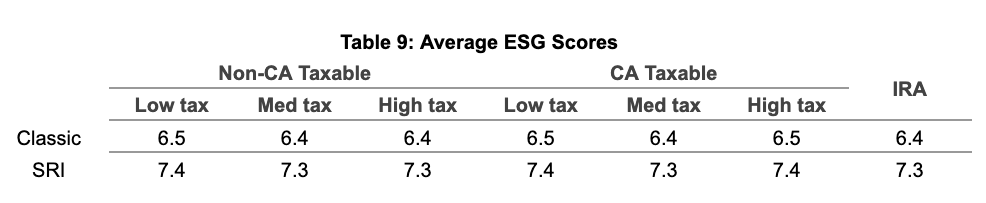

Table 9 takes a simple average across risk scores to arrive at the final average scores for each portfolio type. We see there is a significant improvement in average ESG scores from 6.4 to 6.5 for Classic portfolios to 7.3 to 7.4 for Socially Responsible portfolios.

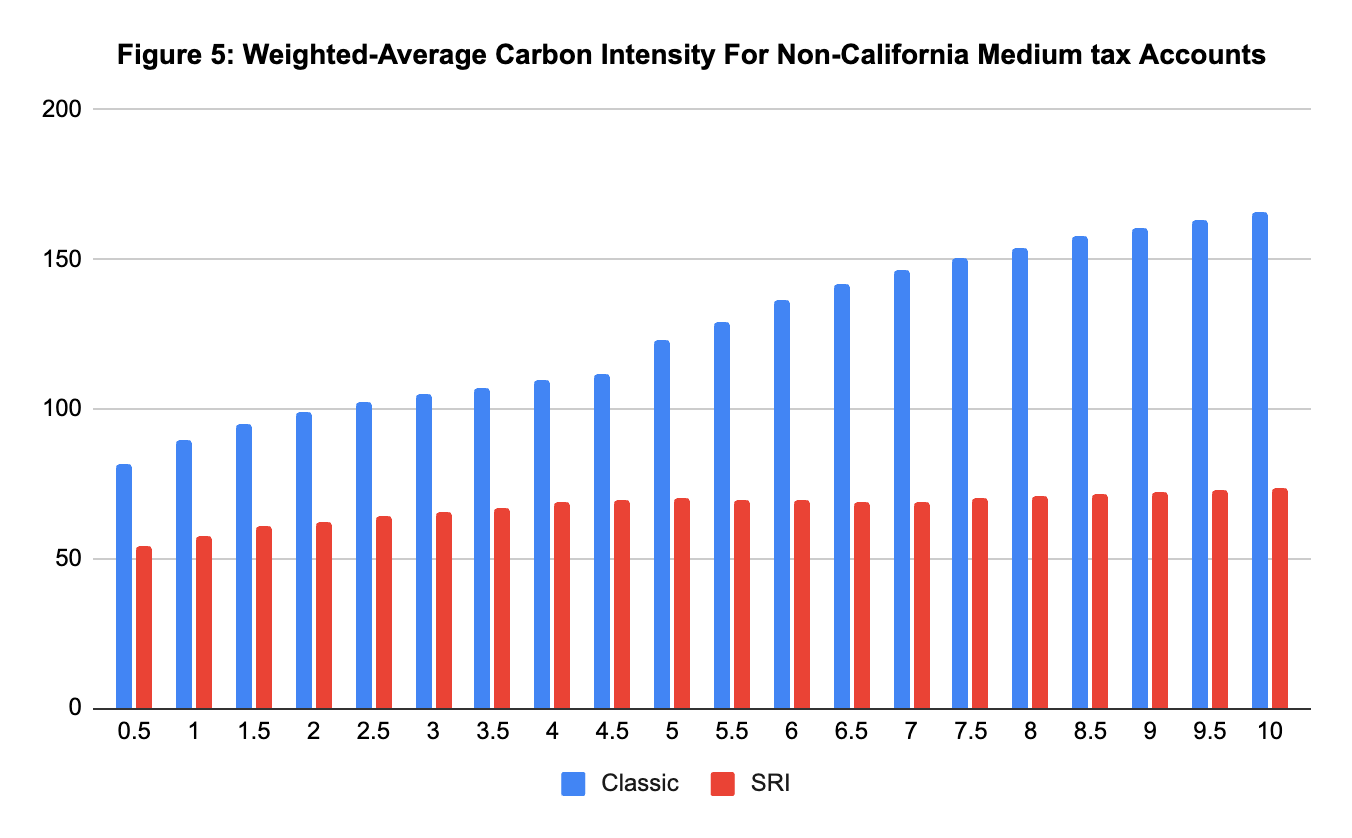

Figure 5 shows the weighted average carbon intensity for non-California medium tax level portfolios. Across the risk scores, Socially Responsible portfolios consistently have significantly lower carbon intensity.

Table 10 takes a simple average across risk scores to show average carbon intensity across portfolio types. As with the ESG score, the Socially Responsible portfolios see a sizable improvement in this metric, from a range of 118 to 131 in the Classic portfolios to a range of 59 to 72 for Socially Responsible portfolios — an average decrease of over 40%.

This average decrease of 61 in carbon intensity scores translates to a decrease of 61 tons of carbon dioxide equivalents for every million dollars sales from companies in the SRI portfolio rather than the Classic portfolio. This is approximately equal to the emissions from thirteen passenger cars or the heating of seven homes for an entire year.

Rebalancing and Ongoing Management

Our Socially Responsible portfolios are managed using the same process as our Classic portfolios, including tax-loss harvesting, dividend reinvestment, and tax-efficient rebalancing and withdrawals.

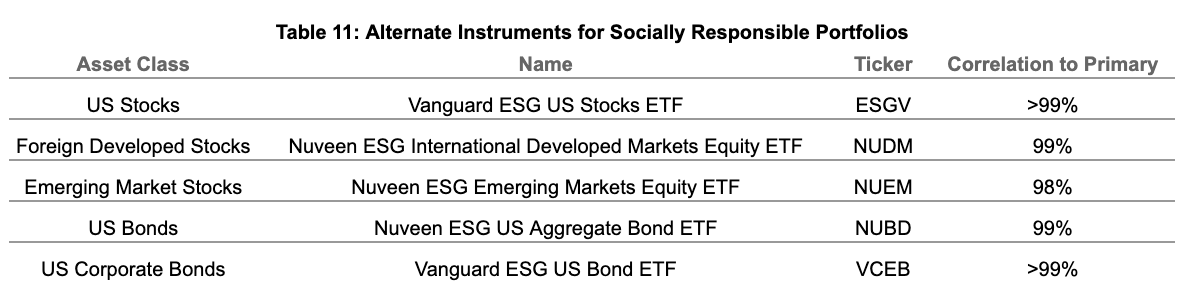

Every ETF used in our Socially Responsible portfolios is eligible for tax-loss harvesting, meaning that Wealthfront clients choosing our SRI option in a taxable account still get the benefit of our tax-loss harvesting service. Table 11 shows the primary and secondary ETFs used for each of the five asset classes where socially responsible funds are available. Each alternate ETF is highly correlated with the primary ETF used to represent the asset class. (Correlations are calculated based on monthly data for the trailing 10 years ending June 30, 2024).

Conclusion

According to MSCI’s robust scoring framework, Wealthfront’s Socially Responsible portfolios show significant improvement in social good and sustainability metrics when compared to our Classic portfolios. At the same time, the Socially Responsible portfolio benefits from the same investment expertise and state-of-the-art asset allocation techniques as our Classic portfolios.

Disclosures

This Wealthfront Investment Methodology White Paper has been prepared by Wealthfront Advisers LLC (“Wealthfront”) solely for informational purposes only. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) any advice or recommendation to purchase any securities or other financial instruments and may not be construed as such. The information set forth herein has been obtained or derived from sources believed by Wealthfront to be reliable but it is not necessarily all-inclusive and is not guaranteed as to its accuracy and is not to be regarded as a representation or warranty, express or implied, as to the information’s accuracy or completeness, nor should the attached information serve as the basis of any investment decision. The information set forth herein has been provided to you as secondary information and should not be the primary source for any investment or allocation decision. This document is subject to further review and revision.

Certain ETFs available to Wealthfront’s clients are labeled by Wealthfront as “Socially Responsible”. In order to be labeled as socially responsible, an ETF must meet at least one of the following criteria: (1) The ETF tracks an index marketed as seeking to adhere to socially responsible or ESG principles through the selection and weighting of its constituents (2) The ETF tracks an index which specifically excludes companies involved in environmentally destructive businesses such as oil and gas exploration and refining, thermal coal, oil sands, palm oil harvesting, or unsustainable production of forest products (3) The ETF tracks an index which favors companies, via the selection or weighting of its constituents, engaged in businesses related to: clean or renewable energy; electric vehicles or clean transportation; or sustainable agriculture and/or forestry (4) The ETF tracks an index which favors companies, via the selection or weighting of its constituents with policies and practices supporting of empowerment of women, minorities, or members of any disadvantaged class, or the inclusion of women, minorities, or members of any disadvantaged class in leadership positions.

The information in this document may contain projections or other forward-looking statements regarding future events, targets, forecasts or expectations that are based on Wealthfront’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Neither the author nor Wealthfront or its affiliates assumes any duty to, nor undertakes to update forward looking statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) changes in laws and regulations and (4) changes in the policies of governments and/or regulatory authorities. Any opinions expressed herein reflect our judgment as of the date hereof and neither the author nor Wealthfront undertakes to advise you of any changes in the views expressed herein.

Investors may experience different results from the hypothetical expected returns shown. The hypothetical expected returns shown do not represent the results of actual trading using client assets and were calculated by means of a retroactive application of a model designed with the benefit of hindsight. Hypothetical expected returns information have many inherent limitations, some of which, but not all, are described herein. No representation is being made that any client account will or is likely to achieve performance returns or losses similar to those shown herein. There are frequently sharp differences between hypothetical expected returns and the actual returns subsequently realized by any particular trading program. One of the limitations of hypothetical expected returns is that they are generally prepared with the benefit of hindsight. There are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results, all of which can adversely affect actual trading results. Hypothetical expected returns are presented for illustrative purposes only. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in achieving the returns have been stated or fully considered. Changes in the assumptions may have a material impact on the hypothetical returns presented. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) changes in laws and regulations and (4) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results, and any hypothetical returns, expected returns, or probability projections may not reflect actual future performance. There is a potential for loss that is not reflected in the hypothetical information portrayed.

Wealthfront Advisers and its affiliates do not provide legal or tax advice and do not assume any liability for the tax consequences of any client transaction. Clients should consult with their personal tax advisors regarding the tax consequences of investing with Wealthfront Advisers and engaging in these tax strategies, based on their particular circumstances. Clients and their personal tax advisors are responsible for how the transactions conducted in an account are reported to the IRS or any other taxing authority on the investor’s personal tax returns. Wealthfront Advisers assumes no responsibility for the tax consequences to any investor of any transaction.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Please see our Full Disclosure for important details.

Investment management and advisory services are provided by Wealthfront Advisers LLC (“Wealthfront Advisers”), an SEC-registered investment adviser, and brokerage related products, including the Cash Account, are provided by Wealthfront Brokerage LLC, a Member of FINRA/SIPC.

Wealthfront, Wealthfront Advisers and Wealthfront Brokerage are wholly owned subsidiaries of Wealthfront Corporation.

© 2024 Wealthfront Corporation. All rights reserved.